Budgeting for 2026: Cut Monthly Expenses by 20% with Smart Financial Tools

Are you looking to take control of your finances and make a significant impact on your savings in 2026? The goal of cutting your monthly expenses by a substantial 20% might seem daunting, but with the right strategies and smart financial tools, it’s not only achievable but also surprisingly straightforward. This comprehensive guide will walk you through a practical, step-by-step approach to identify unnecessary spending, optimize your budget, and harness the power of technology to achieve your financial freedom.

In today’s dynamic economic landscape, every penny counts. Whether you’re saving for a down payment, planning for retirement, or simply aiming for a more comfortable financial future, reducing your monthly outflow is a cornerstone of effective financial planning. By focusing on how to cut monthly expenses, you’re not just saving money; you’re building resilience, gaining peace of mind, and empowering yourself to reach your long-term financial aspirations.

This article is designed to be your ultimate resource for expense reduction. We’ll explore everything from mindset shifts and initial assessments to advanced budgeting techniques and the best financial tools available. Get ready to transform your financial habits and see a tangible difference in your bank account!

Understanding Your Starting Point: The Essential Financial Audit

Before you can effectively cut monthly expenses, you need to understand exactly where your money is going. This involves a thorough financial audit, a process that might sound intimidating but is crucial for uncovering hidden spending patterns and identifying areas for improvement. Think of it as a financial detective mission where you’re the lead investigator.

Step 1: Gather All Financial Statements

Collect bank statements, credit card statements, loan statements, and any other financial records for the past three to six months. This historical data provides a clear picture of your income and expenditure. Don’t overlook smaller, less frequent transactions; they can add up significantly over time.

Step 2: Categorize Your Spending

This is where the real insights begin. Go through each transaction and assign it to a category. Common categories include:

- Housing (rent/mortgage, utilities, maintenance)

- Transportation (gas, public transport, car payments, insurance)

- Food (groceries, dining out, coffee)

- Utilities (electricity, water, internet, cell phone)

- Insurance (health, car, home)

- Debt Payments (credit cards, student loans)

- Entertainment (subscriptions, movies, hobbies)

- Personal Care (gym, salon, clothing)

- Miscellaneous (unexpected costs, gifts)

Many banking apps and financial tools can automate this categorization, making this step much easier. The goal is to see a clear breakdown of where your money is allocated each month.

Step 3: Identify Fixed vs. Variable Expenses

Understanding the difference between these two types of expenses is key to knowing where you can most easily cut monthly expenses.

- Fixed Expenses: These are costs that generally stay the same each month, such as rent/mortgage payments, loan payments, and insurance premiums. While harder to change in the short term, they’re not impossible to adjust (e.g., refinancing a loan, shopping for better insurance rates).

- Variable Expenses: These fluctuate month-to-month and offer the most immediate opportunities for savings. Examples include groceries, dining out, entertainment, and utilities (if usage varies).

Step 4: Calculate Your Average Monthly Spending

Once everything is categorized, sum up your spending for each category over the period you analyzed and divide by the number of months to get an average. This average provides your baseline for comparison and helps you set realistic reduction targets.

Setting Realistic Goals: How Much Can You Truly Save?

The target is to cut monthly expenses by 20%. Is this realistic for you? Absolutely. While some individuals might find it easier than others, a 20% reduction is an ambitious yet achievable goal for most households. The key is to be strategic and consistent.

The 50/30/20 Rule as a Benchmark

A popular budgeting guideline, the 50/30/20 rule suggests allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. If your current spending on ‘wants’ is significantly higher than 30%, you have a clear area to target for your 20% reduction. Even if you’re already quite frugal, there are always areas for optimization.

By understanding your current spending habits and categorizing them effectively, you’ve laid the groundwork. Now, let’s dive into practical strategies to cut monthly expenses across various categories.

Strategic Expense Reduction: Where to Find Your 20%

Achieving a 20% reduction requires a multi-pronged approach. We’ll tackle different spending categories, offering actionable tips for each. Remember, small changes in multiple areas can quickly add up to your target.

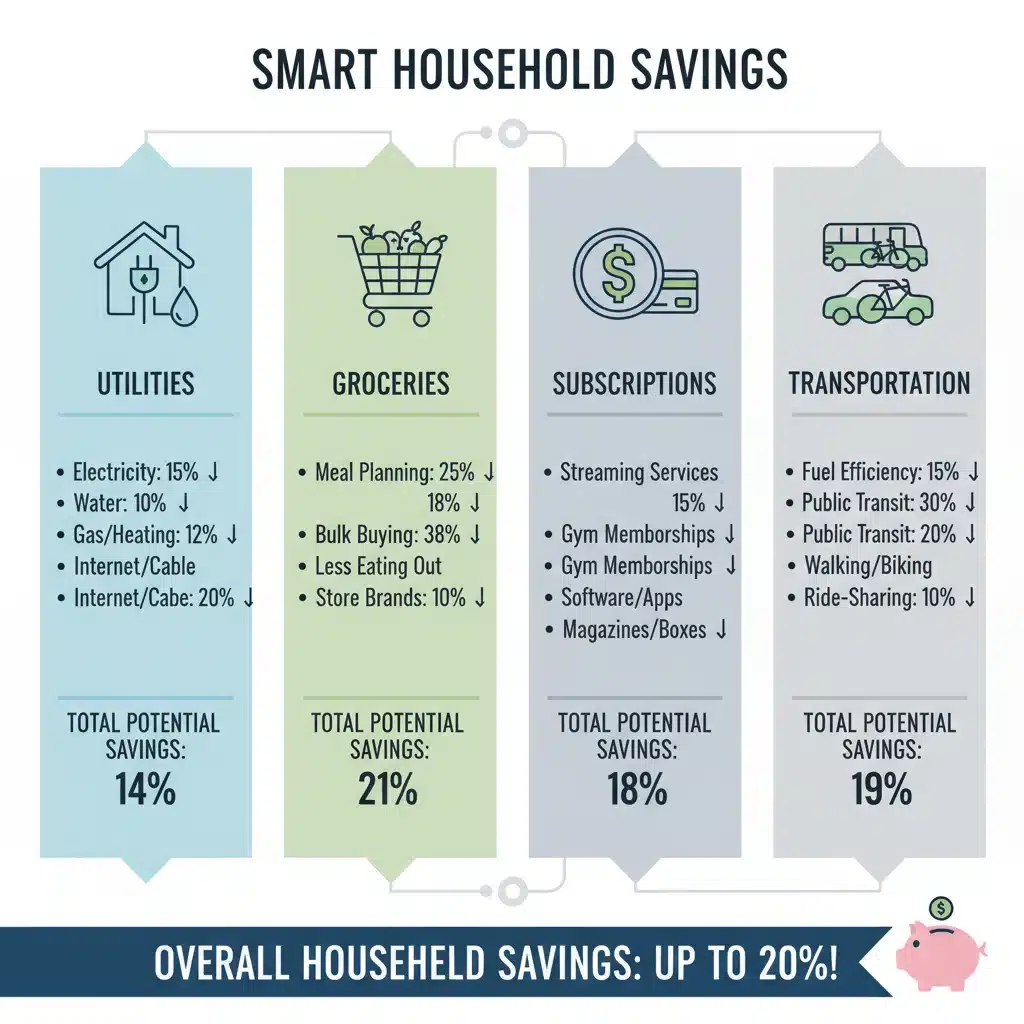

1. Housing and Utilities: The Big Ticket Items

These often represent the largest portion of monthly expenses. While moving might not be an option, there are still ways to save.

- Utilities: Be energy efficient. Unplug electronics, use LED lighting, adjust your thermostat (a smart thermostat can automate this), and take shorter showers. Shop around for better internet or cable packages, or consider cutting the cord entirely. Many providers offer promotional rates for new customers; call your current provider to see if they can match or beat competitors’ offers.

- Rent/Mortgage: If you’re renting, negotiate your lease renewal. If you own, consider refinancing your mortgage if interest rates are favorable, but be mindful of associated fees. Another option, if feasible, is to take on a housemate to split costs.

- Home Maintenance: Tackle small repairs yourself instead of hiring professionals for every little thing. Learn basic DIY skills to save on common household issues.

2. Food: A Flexible Spending Category

Food expenses are notorious for creeping up. This is a prime area to cut monthly expenses significantly.

- Meal Planning: Plan your meals for the week, create a grocery list, and stick to it. This prevents impulse buys and reduces food waste.

- Cook at Home: Eating out, even occasionally, adds up. Pack lunches for work and cook dinners at home more often.

- Shop Smart: Look for sales, use coupons, buy generic brands, and purchase in bulk for non-perishables if you have storage. Avoid shopping when hungry!

- Reduce Food Waste: Learn to repurpose leftovers and properly store food to extend its shelf life.

- Coffee/Drinks: That daily latte habit can cost hundreds a year. Consider making coffee at home or reducing frequency.

3. Transportation: Getting Around on a Budget

Whether you drive, bike, or use public transport, there are ways to save.

- Car Expenses: Combine errands to reduce fuel consumption. Ensure your car is well-maintained to improve fuel efficiency and avoid costly repairs. Shop around for cheaper car insurance annually. Consider carpooling or public transport for your commute.

- Public Transport/Ride-Sharing: Look into monthly passes for public transport which are often cheaper than daily tickets. Limit reliance on expensive ride-sharing services; plan ahead.

- Walking/Biking: For shorter distances, consider walking or biking. It’s free, healthy, and environmentally friendly.

4. Subscriptions and Entertainment: The ‘Death by a Thousand Cuts’ Category

This is often the easiest place to cut monthly expenses without feeling a significant impact on your quality of life.

- Audit Subscriptions: Go through all your recurring subscriptions (streaming services, gym memberships, apps, software). Are you using them all? Cancel those you rarely use. Consider rotating subscriptions – use one streaming service for a few months, then cancel and switch to another.

- Free Alternatives: Explore free entertainment options like public libraries for books and movies, free community events, or outdoor activities.

- Negotiate: Sometimes you can call a service provider and negotiate a lower rate or a temporary pause if you’re not using it.

5. Debt Management: Reducing Interest Payments

While not a direct expense cut, reducing interest payments frees up cash flow, effectively making it easier to cut monthly expenses.

- High-Interest Debt First: Focus on paying off credit card debt or other high-interest loans as quickly as possible. The money saved on interest can be redirected to savings or other financial goals.

- Debt Consolidation: Explore options like a personal loan with a lower interest rate to consolidate multiple high-interest debts.

- Balance Transfers: If you have good credit, a 0% APR balance transfer card can give you time to pay down debt without accruing additional interest (be mindful of transfer fees and the promotional period).

6. Personal Care and Shopping: Mindful Consumption

These categories often involve impulse purchases and can be easily trimmed.

- Clothing: Adopt a ‘buy less, choose well’ philosophy. Shop sales, thrift stores, or consider clothing swaps.

- Beauty/Grooming: Reduce salon visits, learn to do some treatments yourself, or opt for more affordable brands.

- Gifts: Plan ahead for gifts, make handmade gifts, or suggest experience-based gifts to friends and family.

Leveraging Smart Financial Tools to Cut Monthly Expenses

In 2026, you don’t have to tackle budgeting alone. A plethora of smart financial tools can automate, simplify, and optimize your expense reduction efforts. These tools are invaluable for tracking, analyzing, and even predicting your spending patterns, making it easier to cut monthly expenses effectively.

1. Budgeting Apps (e.g., Mint, YNAB, Personal Capital)

- Automatic Tracking: These apps link to your bank accounts and credit cards, automatically categorizing your transactions. This eliminates manual data entry and provides real-time insights into your spending.

- Budget Creation: They help you set spending limits for each category and alert you when you’re approaching or exceeding them.

- Goal Setting: Many apps allow you to set financial goals (e.g., saving for a down payment, paying off debt) and track your progress.

- Net Worth Tracking: Some, like Personal Capital, go beyond budgeting to track your entire net worth, including investments.

2. Expense Trackers (e.g., Expensify, Spendee)

- Detailed Logging: While budgeting apps offer basic tracking, dedicated expense trackers provide more granular control, often with receipt scanning and custom categorization, ideal for freelancers or business owners.

- Visual Reports: They offer intuitive charts and graphs to visualize where your money is going, making it easier to spot areas to cut monthly expenses.

3. Bill Negotiation Services (e.g., Billshark, Trim)

- Automated Savings: These services connect to your accounts and identify recurring bills (internet, cable, cell phone). They then negotiate with providers on your behalf to get lower rates, often without you having to lift a finger.

- Subscription Cancellation: Some can also identify and cancel unwanted subscriptions, directly helping you to cut monthly expenses.

4. Investment and Savings Apps (e.g., Acorns, Betterment, Digit)

- Automated Savings: Apps like Acorns round up your purchases to the nearest dollar and invest the difference. Digit analyzes your spending and automatically saves small amounts when it determines you can afford it, without impacting your daily budget.

- Micro-Investing: These platforms make investing accessible with small amounts, helping you grow your wealth passively.

5. Cash Back and Rewards Apps/Browser Extensions (e.g., Rakuten, Honey)

- Shopping Discounts: While not directly cutting expenses, these tools help you save money on purchases you’re already making by finding coupons, promo codes, and offering cash back. This indirectly contributes to your overall savings.

The Psychology of Saving: Building Sustainable Habits

Cutting expenses isn’t just about numbers; it’s also about changing your mindset and building lasting habits. Understanding the psychology behind your spending can empower you to make smarter financial choices and successfully cut monthly expenses for the long term.

1. The ‘Why’ Behind Your Spending

Take time to reflect on why you spend money in certain categories. Is it out of convenience, habit, social pressure, or emotional reasons? Recognizing these triggers is the first step towards changing unwanted spending behaviors.

2. Delayed Gratification

The ability to resist immediate rewards for greater long-term benefits is crucial for saving. Instead of impulse buying, implement a 24-hour (or even 7-day) rule for non-essential purchases. This pause often reveals whether you truly need or want an item.

3. Gamify Your Savings

Make saving fun! Challenge yourself to a ‘no-spend’ day or week. Set small, achievable goals and reward yourself (non-financially) when you hit them. Many budgeting apps incorporate gamification elements to keep you motivated.

4. Find Cheaper Alternatives

Instead of completely depriving yourself, look for more affordable ways to enjoy your favorite activities or products. Love coffee? Brew it at home. Enjoy movies? Explore free streaming services or library rentals. This approach makes expense reduction feel less like deprivation and more like smart optimization.

5. The Power of Automation

Automate your savings and bill payments. Set up automatic transfers from your checking to your savings account immediately after payday. This ‘pay yourself first’ strategy ensures your savings grow consistently without you having to think about it. Automation is a powerful tool to reinforce your efforts to cut monthly expenses.

6. Track Your Progress and Celebrate Wins

Regularly review your budget and celebrate your achievements, no matter how small. Seeing your savings grow and your debt shrink is incredibly motivating. Use your budgeting tools to visualize your progress; charts and graphs can be powerful motivators.

Navigating Challenges and Staying Motivated

Even with the best intentions and tools, there will be times when you face challenges. Unexpected expenses, social pressures, or simply a lapse in discipline can derail your efforts. Here’s how to stay on track when trying to cut monthly expenses:

1. Build an Emergency Fund

One of the best ways to prevent unexpected costs from derailing your budget is to have an emergency fund. Aim for 3-6 months’ worth of living expenses saved in an easily accessible, high-yield savings account. This fund acts as a buffer against unforeseen circumstances like job loss, medical emergencies, or car repairs.

2. Be Flexible and Adjust

Your budget isn’t set in stone. Life happens, and your financial situation might change. Review your budget regularly (monthly or quarterly) and adjust it as needed. If one category is consistently over budget, see if you can trim another or find ways to reduce spending in that category more effectively.

3. Don’t Deprive Yourself Completely

Extreme austerity often leads to burnout and a complete abandonment of financial goals. Allow yourself small, planned indulgences. Factor ‘fun money’ into your budget in moderation. This makes the process of cutting expenses more sustainable and enjoyable.

4. Seek Support and Accountability

Share your financial goals with a trusted friend, family member, or partner. Having an accountability partner can provide encouragement and help you stay motivated. There are also online communities and forums dedicated to budgeting and saving where you can find support and advice.

5. Focus on the Long-Term Benefits

Remind yourself why you started. Is it for financial freedom, a down payment, or early retirement? Keeping your long-term goals in sight can provide the motivation needed to overcome short-term temptations and continue your efforts to cut monthly expenses.

Conclusion: Your Path to Financial Empowerment in 2026

Successfully cutting your monthly expenses by 20% in 2026 is an ambitious yet entirely achievable goal. It requires a combination of self-awareness, strategic planning, consistent effort, and the smart application of modern financial tools. By conducting a thorough financial audit, setting realistic goals, implementing targeted reduction strategies across various spending categories, and leveraging technology, you can dramatically improve your financial health.

Remember that this journey is not about deprivation, but about optimization and mindful spending. It’s about making conscious choices that align with your financial goals and values. The habits you build now will serve you for years to come, leading to greater financial security and peace of mind.

Start today. Choose one area to focus on first, download a budgeting app, or simply track your spending for a week. Small steps lead to big changes. By committing to these strategies, you’re not just aiming to cut monthly expenses; you’re actively building a stronger, more resilient financial future for yourself and your loved ones. Here’s to a financially healthier 2026!

& IRA Contribution Limits")

Contributions Before the December Deadline: 2026 Retirement Blueprint")