Maximize Your 401(k) Contributions Before the December Deadline: 2026 Retirement Blueprint

Maximize Your 401(k) Contributions Before the December Deadline: Your 2026 Retirement Blueprint

As the year draws to a close, many of us begin to reflect on our financial health and future goals. For those planning their retirement, the month of December carries particular significance, especially when it comes to maximizing your 401(k) contributions. The looming December deadline isn’t just another date on the calendar; it’s a critical juncture that can profoundly impact your financial well-being in retirement. This comprehensive guide will delve into why maximizing your 401(k) contributions before this deadline is paramount for your 2026 retirement blueprint, offering actionable strategies, insights into tax benefits, and a clear understanding of the rules and regulations that govern these crucial accounts.

Retirement planning might seem like a distant concern for many, but the truth is, the earlier and more consistently you contribute to your 401(k), the more robust your retirement nest egg will become. The power of compound interest, coupled with the tax advantages offered by 401(k) plans, makes them an indispensable tool in any long-term financial strategy. Failing to maximize your 401(k) contributions each year means leaving potential growth and tax savings on the table, a mistake that can accumulate into significant financial shortfalls over decades.

This article is designed to be your definitive resource for understanding and acting on your 401(k) contributions before the December deadline. We’ll explore the current contribution limits, delve into the often-overlooked catch-up contributions for those aged 50 and over, and discuss the various types of 401(k) plans available. Furthermore, we’ll provide practical steps to assess your current contributions, calculate how much more you can contribute, and strategize ways to find the extra funds. Our goal is to empower you with the knowledge and motivation to make informed decisions that will secure a comfortable and fulfilling retirement.

The Urgency of the December Deadline for Your 401(k) Contributions

Why is December such a crucial month for your 401(k) contributions? Unlike Individual Retirement Accounts (IRAs), where you typically have until the tax filing deadline of the following year to make contributions for the previous year, 401(k) contributions must generally be made by December 31st of the current year. This hard deadline means that any unused contribution room for the year evaporates once the clock strikes midnight on New Year’s Eve. Missing this window means permanently losing the opportunity to contribute that amount for the current tax year, along with the associated tax benefits and potential investment growth.

For those aiming to build a strong 2026 retirement blueprint, understanding this deadline is paramount. Each dollar contributed to your 401(k) before December 31st is a dollar that starts working for you immediately, potentially growing tax-deferred for decades. The compounding effect of these contributions, even small ones, can lead to substantial differences in your retirement savings over time. Consider the opportunity cost: if you have $1,000 of unused contribution room, and your investments grow at an average of 7% annually, that $1,000 could be worth significantly more by the time you retire, not to mention the immediate tax deduction or tax-free growth (in the case of a Roth 401(k)).

Moreover, maximizing your 401(k) contributions can have an immediate impact on your current tax situation. Traditional 401(k) contributions are made with pre-tax dollars, meaning they reduce your taxable income for the current year. This can lead to a lower tax bill or a larger tax refund. For example, if you’re in the 22% tax bracket and contribute an additional $1,000 to your traditional 401(k), you could reduce your tax liability by $220. This immediate tax savings can be a powerful incentive to ensure you hit your maximum contribution limits before the December deadline.

The December deadline is also particularly important for those who have experienced salary increases, bonuses, or unexpected windfalls throughout the year. These additional funds present an excellent opportunity to bolster your 401(k) contributions without significantly impacting your regular budget. By strategically allocating these extra funds to your retirement account, you can quickly reach your annual maximums and supercharge your savings.

Understanding 401(k) Contribution Limits and Catch-Up Provisions

To effectively maximize your 401(k) contributions, you first need to know the rules. The Internal Revenue Service (IRS) sets annual limits on how much you can contribute to your 401(k), and these limits are adjusted periodically for inflation. For the most relevant year in your 2026 retirement blueprint, it’s crucial to be aware of the limits for the current year and anticipate potential adjustments for future years.

Standard 401(k) Contribution Limits

For 2024, the standard employee contribution limit for 401(k), 403(b), and most 457 plans, as well as the Thrift Savings Plan, is $23,000. This is the maximum amount you, as an employee, can contribute from your paycheck. This limit applies to both traditional and Roth 401(k) plans. It’s important to differentiate this from the total contribution limit, which includes employer contributions and can be significantly higher.

Many individuals, especially earlier in their careers, may not be able to contribute the full $23,000. However, the goal should always be to contribute as much as you comfortably can, ideally at least enough to receive any employer matching contributions. Employer matches are essentially free money, and failing to contribute enough to capture the full match is like turning down a guaranteed return on your investment.

Catch-Up Contributions for Those 50 and Over

One of the most valuable provisions for older workers is the catch-up contribution. If you are aged 50 or older by the end of the calendar year, the IRS allows you to contribute an additional amount above the standard limit. For 2024, the catch-up contribution limit is $7,500. This means that if you are 50 or older, you can contribute a total of $30,500 to your 401(k) ($23,000 standard + $7,500 catch-up).

The catch-up contribution is a powerful tool for those who may have started saving for retirement later in life, or who want to accelerate their savings in the years leading up to retirement. It provides an excellent opportunity to significantly boost your 401(k) balance in a relatively short period, taking full advantage of the tax benefits before you begin withdrawing funds. If you are nearing or past your 50th birthday, make sure you are factoring this additional contribution into your December deadline strategy.

Total Contribution Limits (Employee + Employer)

While the employee contribution limits are important, it’s also worth noting the total contribution limits, which include both your contributions and any contributions made by your employer (such as matching contributions, profit-sharing contributions, and non-elective contributions). For 2024, the total amount that can be contributed to a 401(k) plan for an individual, including both employee and employer contributions, is $69,000. For those aged 50 or over, this limit increases to $76,500 with catch-up contributions.

While most employees primarily focus on their own contributions, understanding the total limit can be beneficial. It ensures that your employer’s contributions, combined with yours, don’t accidentally exceed the IRS maximums, which could lead to penalties. Your plan administrator typically handles this, but it’s good to be aware of the overall landscape.

Traditional vs. Roth 401(k): Which One to Maximize?

When you’re looking to maximize your 401(k) contributions, it’s essential to understand the differences between a traditional 401(k) and a Roth 401(k), as each offers distinct tax advantages that can impact your 2026 retirement blueprint.

Traditional 401(k)

A traditional 401(k) allows you to contribute pre-tax dollars, meaning your contributions are deducted from your taxable income in the year they are made. This reduces your current tax bill. Your investments grow tax-deferred, and you only pay taxes when you withdraw the money in retirement. This option is particularly attractive if you expect to be in a lower tax bracket in retirement than you are now. The immediate tax deduction can be a powerful incentive to maximize these contributions before the December deadline.

Roth 401(k)

A Roth 401(k), on the other hand, is funded with after-tax dollars. Your contributions do not reduce your current taxable income, so there’s no immediate tax deduction. However, the major benefit is that your qualified withdrawals in retirement are completely tax-free. This includes both your contributions and all the investment earnings. A Roth 401(k) is often favored by those who expect to be in a higher tax bracket in retirement, or who simply prefer the certainty of tax-free income in their golden years. If you believe tax rates will be higher in the future, maximizing your Roth 401(k) contributions now could be a very smart move.

Which to Choose for Maximizing 401(k) Contributions?

The choice between a traditional and Roth 401(k) depends on your individual financial situation, current and projected tax brackets, and retirement goals. Some employer plans even allow you to contribute to both a traditional and a Roth 401(k) simultaneously, up to the combined annual limit. This can be an excellent strategy for tax diversification, giving you flexibility in retirement.

Regardless of which type you choose, the principle of maximizing your 401(k) contributions before the December deadline remains the same. The key is to get as much money as possible into these tax-advantaged accounts to benefit from their growth potential and tax efficiencies.

Strategies to Maximize Your 401(k) Contributions Before December

Now that you understand the ‘why’ and the ‘what,’ let’s focus on the ‘how.’ Maximizing your 401(k) contributions by the December deadline requires a bit of planning and, for some, a strategic reallocation of funds. Here are several actionable strategies:

1. Review Your Current Contributions

The first step is to assess where you stand. Check your most recent pay stub or log into your 401(k) plan’s online portal to see your year-to-date contributions. Compare this amount against the annual limit (e.g., $23,000 or $30,500 if you’re 50+). Calculate the difference – this is how much more you can contribute before the December deadline.

2. Adjust Your Payroll Deductions

If you discover you’re behind schedule, the most straightforward way to catch up is to increase your payroll deduction for the remaining pay periods in the year. For example, if you have two paychecks left in December and need to contribute an additional $2,000, you’ll need to increase your deduction by $1,000 per paycheck. Contact your HR department or plan administrator to make these adjustments promptly.

3. Utilize Bonuses or Windfalls

Did you receive a year-end bonus, a commission, or an unexpected inheritance? These funds are perfect candidates for boosting your 401(k) contributions. Instead of spending them, consider directing a significant portion (or all) of these extra funds into your retirement account. Many employers allow you to designate a percentage of your bonus for 401(k) contributions.

4. Cut Discretionary Spending

If you don’t have a bonus or windfall, you might need to find the extra cash by temporarily reducing discretionary spending. Look at your budget for November and December. Can you cut back on dining out, entertainment, holiday shopping (perhaps slightly), or other non-essential expenses? Even small adjustments can free up hundreds of dollars to go towards your 401(k) contributions.

5. Consider a Loan or Withdrawal (with caution)

While generally not recommended for maximizing contributions, it’s worth noting that some plans allow you to take a loan from your 401(k). However, borrowing from your retirement savings comes with risks, including potential taxes and penalties if you don’t repay it on time, and the loss of investment growth on the borrowed amount. This strategy should only be considered as a last resort and with careful financial planning. The primary goal is to contribute new money, not re-circulate existing funds.

6. Plan for Next Year Now

Once you’ve maximized your 401(k) contributions for the current year, don’t wait until next December to think about it again. Immediately set up your payroll deductions for the new year to ensure you’re on track to hit the maximum contribution early. A good strategy is to divide the annual limit by the number of paychecks you receive in a year and set your contribution percentage accordingly. This ‘set it and forget it’ approach ensures consistent savings and prevents a last-minute scramble.

The Long-Term Impact: Your 2026 Retirement Blueprint

The decisions you make regarding your 401(k) contributions before this December deadline are not isolated financial actions; they are foundational elements of your 2026 retirement blueprint and beyond. Consistent, maximized contributions have a profound impact on your financial future through several key mechanisms:

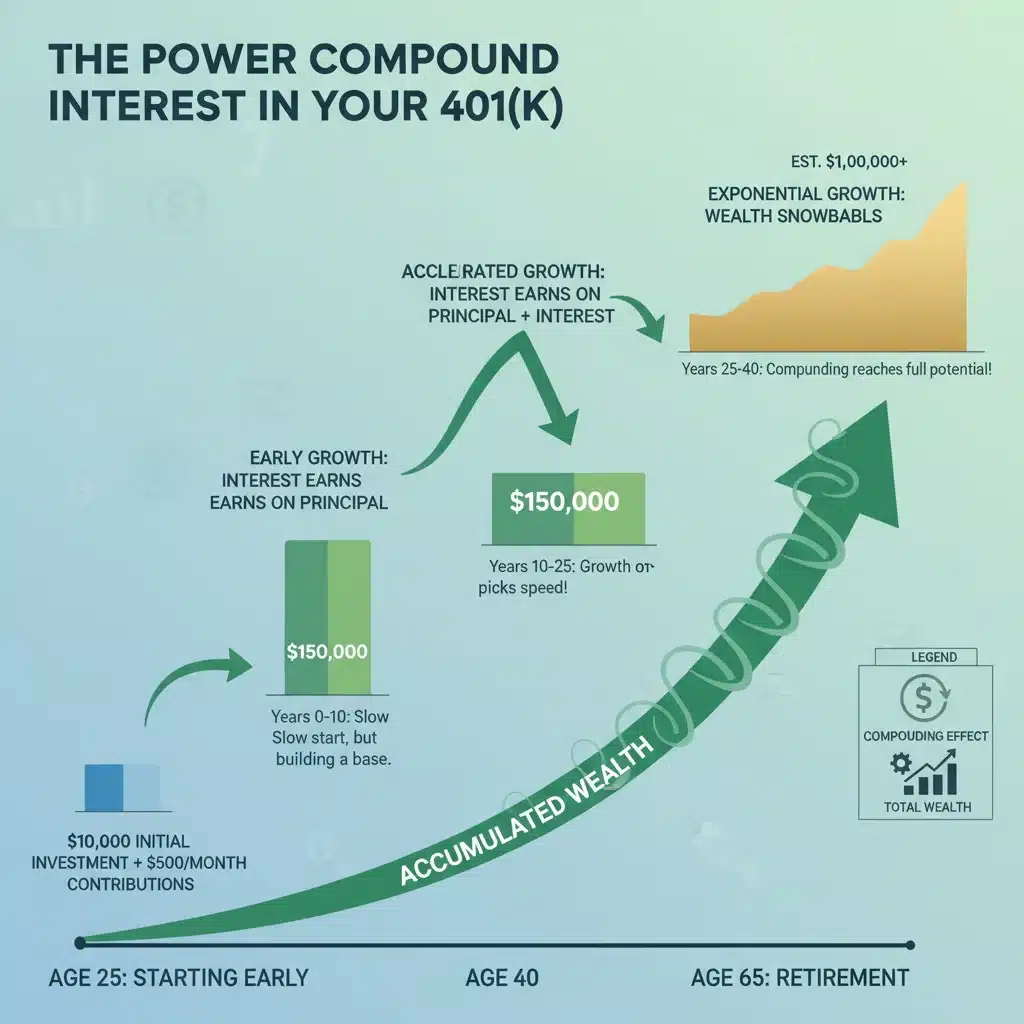

Compound Interest: The Eighth Wonder of the World

Albert Einstein is often attributed with calling compound interest the ‘eighth wonder of the world.’ When you maximize your 401(k) contributions, you are giving more money more time to benefit from this powerful force. Each dollar you contribute starts earning returns, and those returns then start earning returns themselves. Over decades, this snowball effect can transform modest contributions into substantial wealth. Missing even one year of maximized contributions means missing out on years of potential compound growth on those funds.

Tax Advantages: Reducing Your Burden, Increasing Your Savings

Whether you choose a traditional or Roth 401(k), you benefit from significant tax advantages. Traditional 401(k) contributions reduce your current taxable income, potentially lowering your tax bracket and saving you money in the short term. Roth 401(k) contributions, while not offering an upfront deduction, provide tax-free growth and withdrawals in retirement. These tax efficiencies mean more of your money goes towards saving and growing your wealth, rather than being siphoned off by taxes.

Financial Security and Peace of Mind

A well-funded 401(k) provides a strong foundation for financial security in retirement. It reduces reliance on Social Security, allows for a more comfortable lifestyle, and offers the peace of mind that comes from knowing you have adequately prepared for your future. Maximizing your 401(k) contributions is a direct step towards achieving these goals, ensuring you have the resources to enjoy your retirement years without undue financial stress.

Flexibility and Options in Retirement

The more you save, the more options you’ll have in retirement. A larger 401(k) balance can mean the ability to retire earlier, pursue hobbies or travel, cover unexpected medical expenses, or even leave a legacy for your loved ones. By diligently maximizing your 401(k) contributions, you are essentially investing in your future freedom and flexibility.

Common Misconceptions and FAQs About 401(k) Contributions

Despite their importance, 401(k) plans are often misunderstood. Let’s address some common questions and misconceptions that might prevent individuals from maximizing their 401(k) contributions.

"I can’t afford to maximize my 401(k) contributions."

This is a common sentiment, but it’s crucial to reframe your perspective. Think of your 401(k) contributions as paying your future self. Even small increases can make a big difference over time. Start by contributing at least enough to get your employer’s full match – that’s a 100% return on your investment, guaranteed. Then, aim to increase your contribution by just 1% or 2% of your salary each year. You might be surprised how quickly you adapt to the slightly smaller take-home pay, especially when you consider the tax benefits.

"It’s too late to start maximizing my contributions."

It’s never too late to improve your retirement savings strategy. While starting early is ideal, every year you contribute more, especially taking advantage of catch-up contributions if you’re 50+, significantly boosts your retirement funds. The December deadline is a perfect opportunity to make a substantial impact, even if you’re catching up.

"My employer’s 401(k) plan isn’t very good."

While some 401(k) plans offer better investment options or lower fees than others, contributing to any 401(k) is almost always better than not contributing at all, especially if there’s an employer match. The tax advantages alone make it a worthwhile vehicle for retirement savings. If you’re concerned about the quality of your plan, focus on maximizing your contributions to get the tax benefits and employer match, and then consider other investment vehicles like an IRA or a taxable brokerage account for additional savings.

"I’ll just save more next year."

This is a dangerous mindset. As discussed, the December deadline means that contribution room for the current year is lost forever. You can’t go back and contribute for a past year to your 401(k). Procrastination not only means missing out on tax benefits but also losing valuable time for your investments to grow through compounding. Make the most of the current year’s opportunity.

"What if I need the money before retirement?"

While 401(k)s are designed for retirement, there are provisions for early withdrawals in certain circumstances (e.g., hardship withdrawals), though these often come with penalties and taxes. Some plans also allow for 401(k) loans. However, it’s generally best to avoid tapping into your retirement savings early. Building a separate emergency fund is crucial so you don’t have to rely on your 401(k) for short-term needs.

Conclusion: Act Now to Secure Your 2026 Retirement Blueprint

The December deadline for maximizing your 401(k) contributions is not just a financial task; it’s a strategic imperative for anyone serious about building a robust 2026 retirement blueprint and securing their financial future. The combination of tax advantages, the power of compound interest, and the irreversible nature of the annual contribution window makes this period exceptionally critical.

By taking the time now to review your year-to-date contributions, understanding the limits (including catch-up provisions if applicable), and implementing strategies to bridge any gaps, you can ensure you’re making the most of this invaluable retirement savings vehicle. Whether it’s adjusting your payroll, funneling a year-end bonus, or temporarily tightening your belt, the effort you put in now will pay dividends for decades to come.

Don’t let this December deadline pass you by without a concerted effort to maximize your 401(k) contributions. Your future self will thank you for the foresight, discipline, and strategic planning you demonstrate today. Start planning, take action, and cement a stronger, more secure retirement for yourself.

& IRA Contribution Limits")